Commodity-Based Pseudo Firms

Consider a pseudo firm that purchases one unit of a commodity, such as one barrel of oil or one ounce of gold, by issuing equity and a zero-coupon bond with face value K and maturity T.

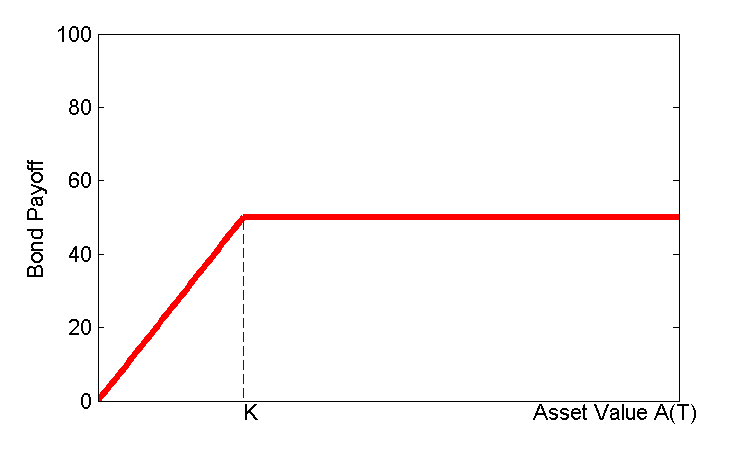

Bond holders have a payoff at time T equal to

Payoff Bond Holders = min(A(t), K) = K - max(K - A(t), 0)where A(t) = commodity price at time t. The payoff profile is the following:

For concreteness, consider a "oil-based" pseudo firm, for instance. The value of the zero coupon bond “issued” by such firm is then B(t,T) = K Z(t,T) - POil(K,t,T) where

- Z(t,T) = price of a Treasury zero coupon bond;

- POil(K,t,T) = price of a put option on oil

Above, E(t) stands for equity value, which in this framework can be computed as a residual from the accounting identity Assets = Liabilities.

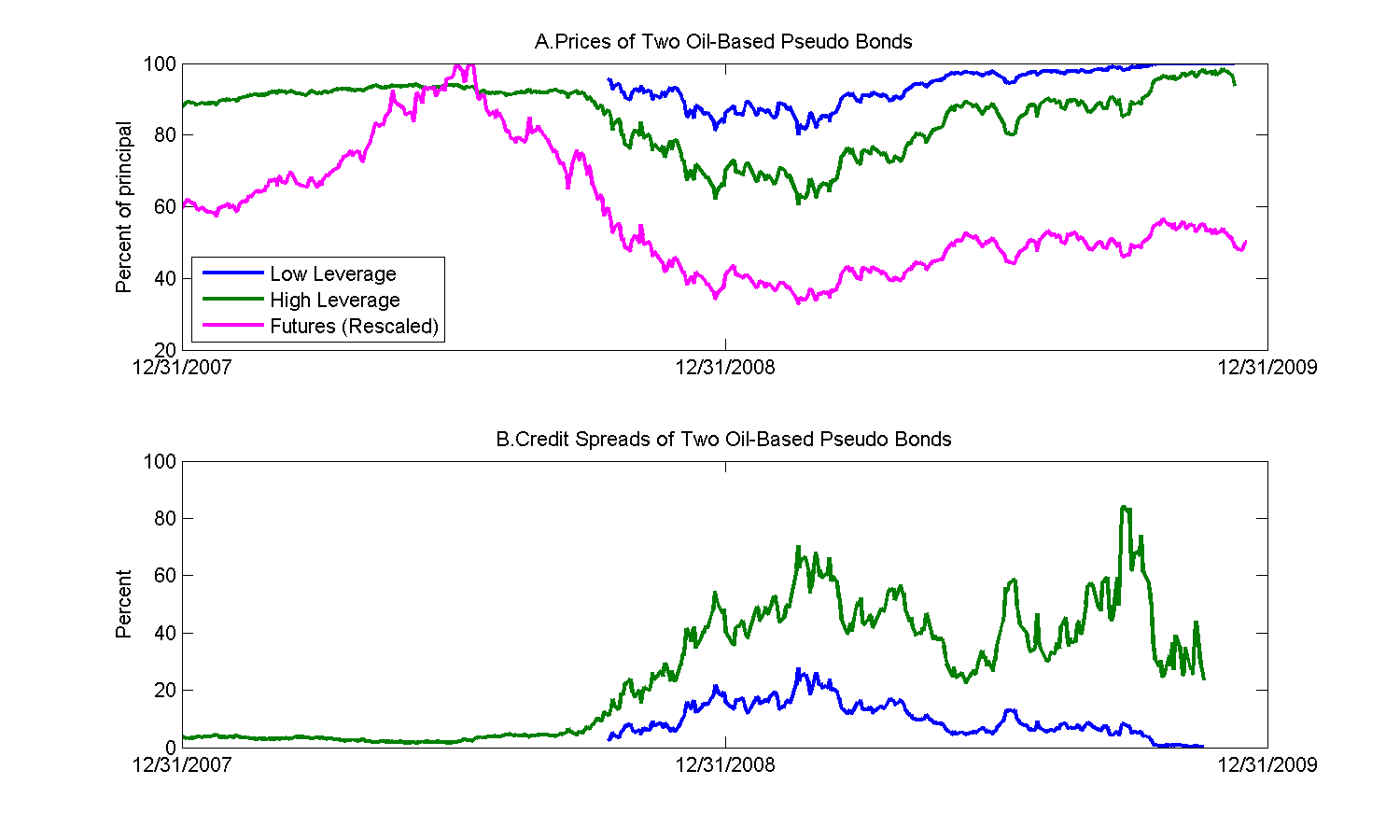

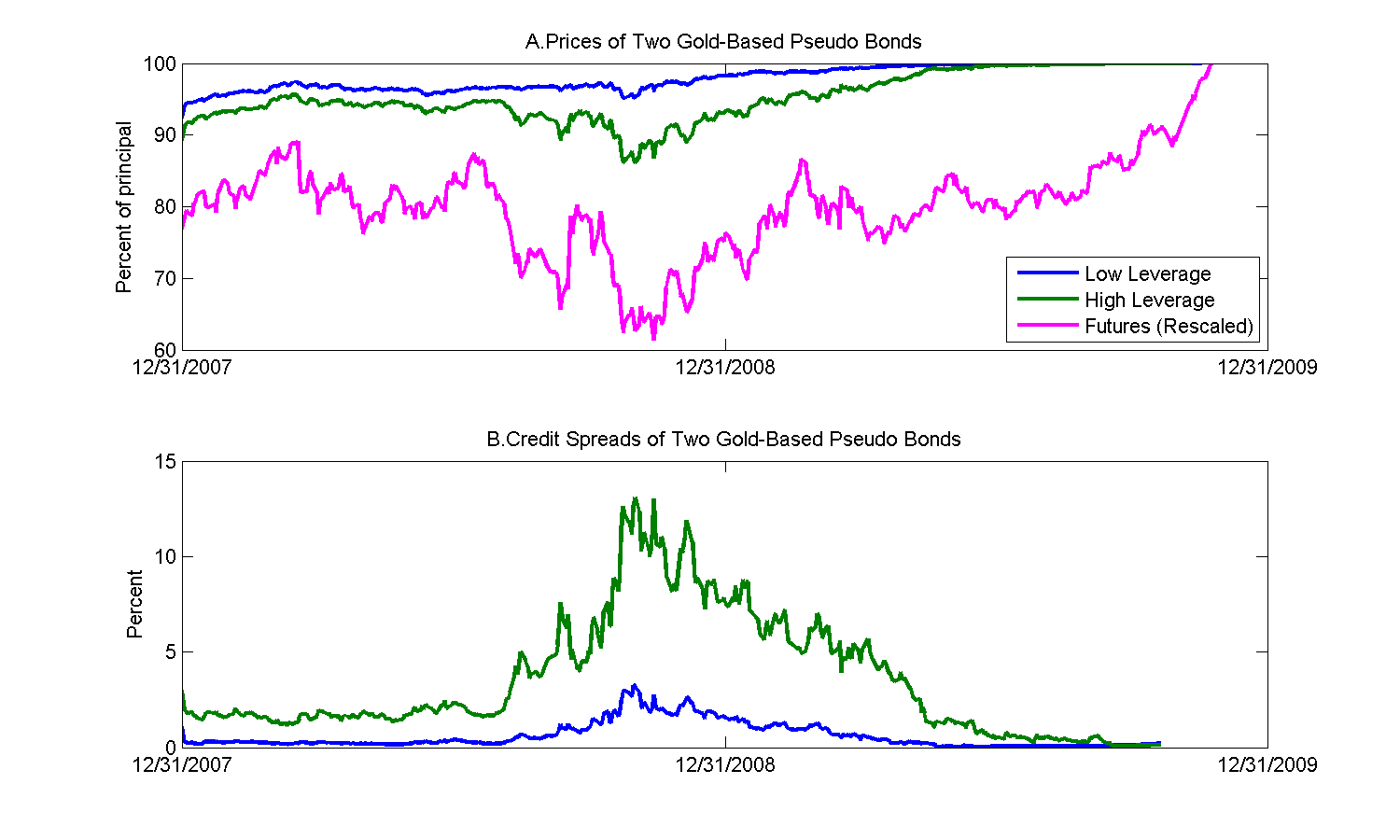

Application: Oil- and Gold-Based Pseudo Firms during the Crisis.

(data from Culp, Nozawa, Veronesi (2015)):

To make the framewory operational, we need commodity options. Unfortunately, data on commodity options are not available. We use CME data on put options on commodity futures. If the option expires at the same time as the futures, the payoff of such put option on futures is exactly max(K - A(T), 0). Therefore, the observable value of such put options on futures can be used for our analysis.

The next two figures report the bond prices (Panels A) and the credit spreads (Panels B) of two commodity-based pseudo firms, whose assets are either "Oil" or "Gold".

Panels A and B of these figures plot the following quantities:

- Panels A plot the prices of a low leverage and a high leverage pseudo bond "issued" by the pseudo firms from June 2007 to November 2009. In each case, we also plot the (rescaled) underlying futures. In both figures, the low-leverage pseudo bond price steadily increases over time -- like any zero-coupon bond -- except during the 2008 crisis, when it drops substantially. Still, this pseudo bond eventually pays 100\% of principal at maturity. The pseudo bond issued by the high-leverage firm instead displays a larger price drop during the financial crisis, which in the case of oil never fully recovers (while it does for gold). The oil-based pseudo firm eventually defaults and bond holders would only receive the ``recovery amount'' A(T)/K2.

- Panels B plot the credit spreads of the pseudo bonds issued by these firms. The high-leverage pseudo bonds always has higher credit spreads than the low-leverage pseudo bonds. Credit spreads are low initially but increase during the financial crisis. The credit spread of the low-leverage pseudo bonds then converges back to a negligible number by the end of the sample, whereas the oil-based, high-leverage pseudo bond displays credit spreads of over 80% as it nears maturity.